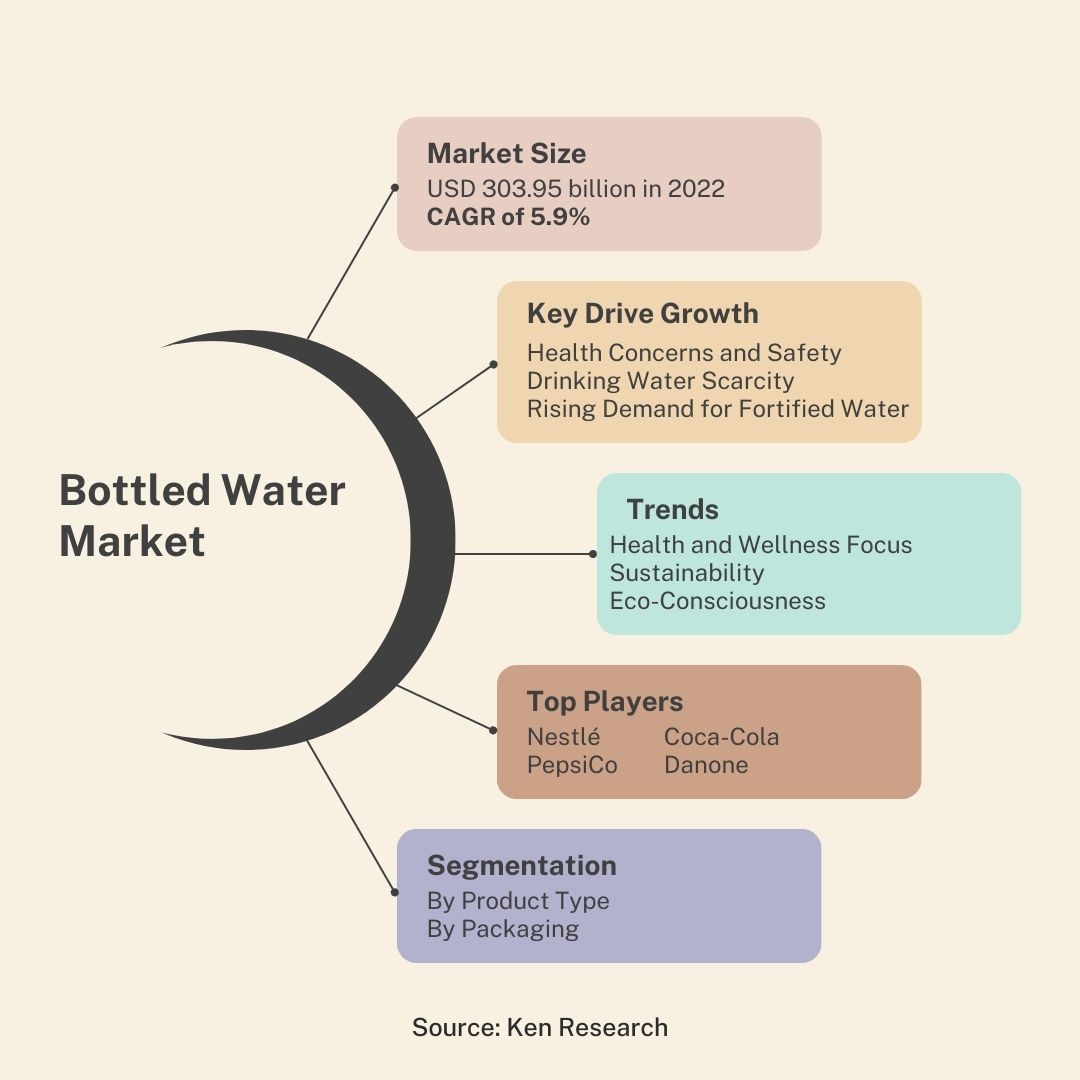

In 2022, the global bottled water market was valued at an impressive USD 303.95 billion. Projections indicate that the market will grow at a compound annual growth rate (CAGR) of 5.9% from 2023 to 2030. This growth is driven by several factors, including health concerns, drinking water scarcity, and a rising demand for nutrient-fortified water.

Bottled Water Market Key Drive Growth

Here are some of the key factors driving this growth

Health Concerns and Safety

One of the primary drivers of the bottled water industry is the increasing concern over health and safety. Consumers are more aware of the potential health risks associated with contaminated water. Diseases such as dysentery, diarrhea, and typhoid, often linked to poor water quality, have pushed consumers towards safer, bottled alternatives.

Drinking Water Scarcity

In many parts of the world, access to clean drinking water is a significant issue. This scarcity has made bottled water a necessity in regions where safe tap water is not available, driving up the demand and sales of bottled water products.

Rising Demand for Fortified Water

The trend towards health and wellness has also spurred demand for nutrient-fortified bottled water. Consumers are increasingly looking for water that not only hydrates but also provides additional health benefits. This includes alkaline water, electrolyte-rich water, and other fortified options.

Trends in the Bottled Water Industry

The bottled water market is experiencing a wave of change, driven by factors like health consciousness, sustainability concerns, and consumer preferences.

Health and Wellness Focus

Functional Water Boom: Regular bottled water is still king, but functional water infused with electrolytes, vitamins, or minerals is witnessing the fastest growth. Consumers are looking for beverages that go beyond hydration and support specific health goals.

Nutrient Fortification: This trend caters to the growing demand for healthy alternatives to sugary drinks. Bottled water with added benefits like antioxidants or immunity boosters is gaining traction.

Sustainability and Eco-Consciousness

Shifting Packaging: Consumers are increasingly concerned about plastic waste. This is leading to a rise in the use of recycled PET (rPET) bottles and a growing interest in alternative packaging solutions like aluminum cans.

Water Footprint Awareness: Companies are focusing on water conservation efforts throughout the production cycle to minimize their environmental impact.

Convenience and Consumer Preferences

Single-Serve Dominance: Smaller, single-serving bottled water remains the most popular format due to its portability and convenience, especially for on-the-go consumption.

Premiumization: Consumers are willing to pay more for premium bottled water brands that offer unique flavors, sourcing, or perceived health benefits.

Rise of On-Trade Consumption: Bottled water sales in restaurants, cafes, and other foodservice establishments are growing as consumers seek convenient hydration options while dining out.

Regional Variations

Asia Pacific Leads the Way: This region is the biggest bottled water sector due to growing populations, rising disposable incomes, and increasing awareness about hygiene and health.

Sustainability Focus in Europe: European consumers are driving the demand for eco-friendly packaging solutions and water sources with minimal environmental impact.

North American Trends: The focus in North America remains on convenience and healthy alternatives to sugary drinks. Functional water and single-serve options continue to be popular choices.

Top Players in the Bottled Water Market

The bottled water sector is dominated by a mix of global giants and regional players.

Global Beverage Companies

Nestlé: A household name, Nestlé owns popular bottled water brands like Perrier and San Pellegrino.

PepsiCo: Owns the Aquafina brand, a major player in the purified bottled water segment.

The Coca-Cola Company: Owns Dasani, another leading brand in purified bottled water.

Danone: Owns the Evian brand, known for its natural spring water sourced from the French Alps.

Other Major Players

Nongfu Spring (China): A leading bottled water company in China, known for its focus on high-quality natural spring water.

Primo Water Corporation (US): A leading provider of home and office water delivery services in the US.

FIJI Water Company LLC (Fiji): Known for its premium bottled water sourced from artesian wells in Fiji.

National Beverage Corp. (US): Owns the La Croix brand, a popular sparkling water brand with a significant bottled water presence.

Keurig Dr Pepper Inc. (US): Owns the Poland Spring brand, a major player in the Northeast US bottled water market.

Market Segmentation

The bottled water sector is segmentation across several key categories to understand consumer preferences, product offerings, and market dynamics.

By Product Type

Still Water: This is the most popular and largest segment, accounting for over 74.5% of the market share. It offers a pure and basic option for hydration.

Sparkling Water: Carbonated bottled water is gaining traction, particularly with the rise of flavored varieties.

Functional Water: This segment includes water infused with electrolytes, vitamins, minerals, antioxidants, or other additives for perceived health benefits. It's the fastest-growing category due to the focus on health and wellness.

By Packaging

PET (Polyethylene Terephthalate): The most dominant packaging material due to its low cost and lightweight nature. However, concerns about plastic waste are pushing for alternatives.

Glass Bottles: While offering a more premium feel and reusability, glass is heavier and more expensive, limiting its market share.

Aluminum Cans: Gaining popularity due to their superior protection against light and air, potentially improving water quality and taste.

By Distribution Channel

Off-Trade: This includes supermarkets, hypermarkets, convenience stores, and other retail outlets. It accounts for the largest share of the market due to convenience and ease of purchase.

On-Trade: Bottled water sold in restaurants, cafes, and other foodservice establishments. This segment is growing as consumers seek convenient hydration options while dining out.

Challenges in the Bottled Water Sector

The bottled water industry, despite its projected growth, faces several challenges that need to be addressed.

Environmental Concerns

Plastic Pollution: Plastic waste from discarded bottles is a major environmental issue. Consumers are becoming increasingly conscious of this problem, putting pressure on the industry to find more sustainable packaging solutions.

Water Scarcity: Bottled water production can put a strain on freshwater resources, especially in areas already facing water scarcity. Companies need to demonstrate responsible water sourcing practices.

Energy Consumption: The production, transportation, and recycling of plastic bottles require significant energy consumption, contributing to greenhouse gas emissions.

Cost and Consumer Perception

High Cost Compared to Tap Water: Bottled water can be significantly more expensive than tap water, especially when considering the environmental impact. This can lead to consumer resentment and a push for improved tap water quality.

Perception of Bottled Water as "Healthier": The belief that bottled water is inherently healthier than tap water is often unfounded. In many cases, tap water undergoes rigorous treatment and meets safety standards.

Competition

Rise of Reusable Bottles and Filtration Systems: Consumers are increasingly opting for reusable water bottles and home filtration systems as a more sustainable and cost-effective alternative.

Focus on Tap Water Improvement: Governments and municipalities are investing in improving tap water quality and infrastructure, potentially reducing reliance on bottled water.

Conclusion

The bottled water sector is poised for continued growth, driven by health concerns, innovation, and expanding markets. Companies that can navigate the challenges and capitalize on the opportunities will thrive in this dynamic industry.